- The Data Tapes

- Posts

- The Data Tapes

The Data Tapes

Setpoint's Bite-Sized Debt Newsletter: May Edition I

The Latest in ABS and Debt Markets

Welcome to The Data Tapes—your biweekly snapshot of private credit and ABS markets. In each edition, we bring you concise updates on debt financings, platform fundraises, data insights, market trends, and the latest from Setpoint.

🚀 What’s New at Setpoint

🔍 The Verification Agent Question Capital Providers Aren’t Asking: When you buy a house, you don't trust the appraiser the seller recommends; so why do capital providers let borrowers choose their verification agent? More from Setpoint’s SVP of Growth, Bart Steenbergen, on why capital providers should rethink how verification agents get selected: 2 min read.

💡 The Most Important Financial Institution Nobody Talks About Anymore: GE Capital was a $600B lending platform that shaped the ABF playbook Apollo, Ares, KKR, and others still run today. It’s been dead for five years, but its influence on the architecture of modern private credit is everywhere. More from Business Development & Partnerships Lead at Setpoint, Conor Witt, here.

🌆 Upcoming Setpoint Events:

LAST CHANCE | Private Credit's Next Act — May 12: Join Setpoint and Blue Owl for a private panel discussion and happy hour at a16z’s San Francisco office. Apply to attend.

Capital Conversations Summer Kickoff — June 2: Join Setpoint and Cross River for Capital Conversations, a happy hour bringing together the asset-backed finance community in NYC. Whether you're an investor, capital provider, or borrower, this is a chance to connect with industry leaders, exchange ideas, and enjoy great cocktails and bites. Apply to attend.

🤝 We're on the road — let's connect:

Secondary and Capital Markets Conference, May 17-20 — New York, NY | Meet with us.

IMN's Residential Mortgage Securitization, June 3 — New York, NY | Meet with us.

IMN's SFR East, May 18-20 — Miami, FL | Meet with us.

💸 Debt Financings & Acquisitions

Aspire, an RMBS investment firm, closed a $450M ABS issuance backed by a pool of mortgages.

Bertelsmann SE, a German media business, agreed to buy Concord, an independent music group and catalog acquisition company. The combined company is valued at $14B.

Best Egg, a consumer finance platform, announced the completion of its acquisition by Barclays.

Better Home & Finance Company, a mortgage and home equity finance platform, launched the Better Home Equity Card to offer homeowners prepaid debit access to funds drawn from a secured Better HELOC.

Castlelake, an alternative asset manager, announced a strategic JV with Redwood Trust to purchase up to $8B of Sequoia-sourced prime jumbo loans.

Castlelake, an alternative asset manager, acquired a majority stake in Resfin Partners, which owns and operates Eastview, a US mortgage correspondent business and Lendmarq, an RTL origination platform.

Consumer Portfolio Services, a consumer auto platform, closed a $514.07M ABS issuance.

Deepinfra, a cloud inference platform for high throughput AI, closed a $107M combined equity and debt financing from 500 Global, Felicis, NVIDIA, Peak6, and Upper90.

Doc2Doc, a financial services platform for healthcare providers, closed a $150M credit facility to scale origination capacity.

GLS, a consumer auto finance platform, closed a $1.1B ABS issuance secured by a pool of subprime auto loans.

Idea Financial, a small business finance platform, closed a $175M asset-backed credit facility with Pinnacle Financial Partners and MA Asset Management to scale origination volume.

Kapitus, a small business finance platform, closed a $150M ABS issuance backed by a pool of revolving small business loans.

Kashable, an employer-sponsored personal loan platform, closed a $60M Series C financing led by Goldman Sachs Alternatives’ Sustainable Investing.

Keystone, a credit fund, closed a $25M senior secured credit facility with a small business finance company to finance origination volume.

Lendmark, a consumer finance platform, closed a $300M ABS issuance secured by a pool of personal loans.

Lobel Financial, a consumer auto finance platform, closed a $223.8M ABS issuance secured by a pool of subprime auto loan contracts financing used cars, trucks, minivans, and SUVs.

OppFi, a consumer finance platform, announced an agreement to acquire BNCCORP Inc. and its wholly owned subsidiary, BNC National Bank, in a cash and stock deal worth approximately $130M.

Point, an HEI originator, closed a partnership with Tacora Capital to sell up to $300M of home equity investment contracts.

Power Home Remodeling, an exterior home remodeler, closed a growth investment from Bain Capital, Sixth Street, and Harvest Partners Structured Capital.

Roc360, a vertically integrated real estate lending and investment management firm, closed a $150M investment from Temasek to increase lending capacity and scale its RTL volume.

SoFi, a consumer finance platform and bank, closed a $688.5M ABS issuance secured by a static pool of unsecured near-prime consumer loans.

TowerPoint Infrastructure Partners, a digital infrastructure and telecom platform, closed a $386M ABS issuance.

Tropical Smoothie Cafe, a restaurant franchise, closed a $270M ABS issuance backed by existing and future franchise and licensing agreements.

Upstart, an AI lending marketplace and consumer finance platform, closed a $1.25B forward flow commitment with Fortress to buy consumer loans originated through Upstart over 15 months. Upstart also closed a $1.2B forward flow agreement with Centerbridge Partners.

Vertical Bridge, the largest owner of communications infrastructure in the US, announced a $1.5B strategic equity investment from KKR.

Watercress Financial, a home improvement financing platform, closed a $550M forward flow partnership with 26North to purchase loans originated through Watercress’s contractor network.

💰️Platform Growth

Apollo closed Accord Fund VII with $1.9B in commitments to invest in dislocated liquid credit opportunities. Apollo also raised $6.5B in total commitments for Apollo Hybrid Value Fund III to invest in structured equity opportunities and capital solutions with equity participation.

Blackstone launched Blackstone N1, folding its Blackstone Growth business into a new unit focused on its AI portfolio.

Crescent Cove, an asset manager, closed Crescent Cove Fund IV with $446M in commitments to provide growth capital solutions to technology companies.

Dime Community Bank launched an Equipment and Franchise Finance group to serve middle-market companies and experienced franchise operators.

Domain Capital Group launched its Sports Credit Strategy and closed an SMA focused on receivables tied to European football player transfers and media rights, following the close of Domain Entertainment Fund II with $768M in commitments.

Hunter Point announced a strategic partnership with Sumitomo Mitsui Trust Bank.

Lazard, a financial advisory and asset management firm, announced its acquisition of Campbell Lutyens, a private capital advisory firm, for $575M.

LibreMax, an alternative asset manager, launched LibreMax Asset-Backed Income Fund (LMIFX), an interval fund providing access to private asset-backed finance and traded structured credit opportunities, with $285M of initial capital.

Neuberger Berman East Asia Limited, the Japan-based entity of Neuberger Berman, announced a JV with Sumitomo Mitsui Banking Corporation to manage private debt funds investing in LBO senior loans.

Pioneer Bancorp, a financial holding company, acquired Targeted Lending Co, LLC, an independent equipment finance company with $120M of loans on its balance sheet.

Primary Wave, an independent music publisher and catalog owner, closed its latest music royalties fund, Primary Wave Music IP Fund 4 with $2.225B in commitments.

Silver Rock Capital Partners, an alternative credit asset manager, closed over $4B in investable capital for its Tactical Allocation Strategy to provide capital solutions across corporate debt and real assets.

StepStone Group, a global investment firm, closed StepStone Credit Opportunities Fund II with $1.58B in commitments to invest across credit secondaries and co-investments.

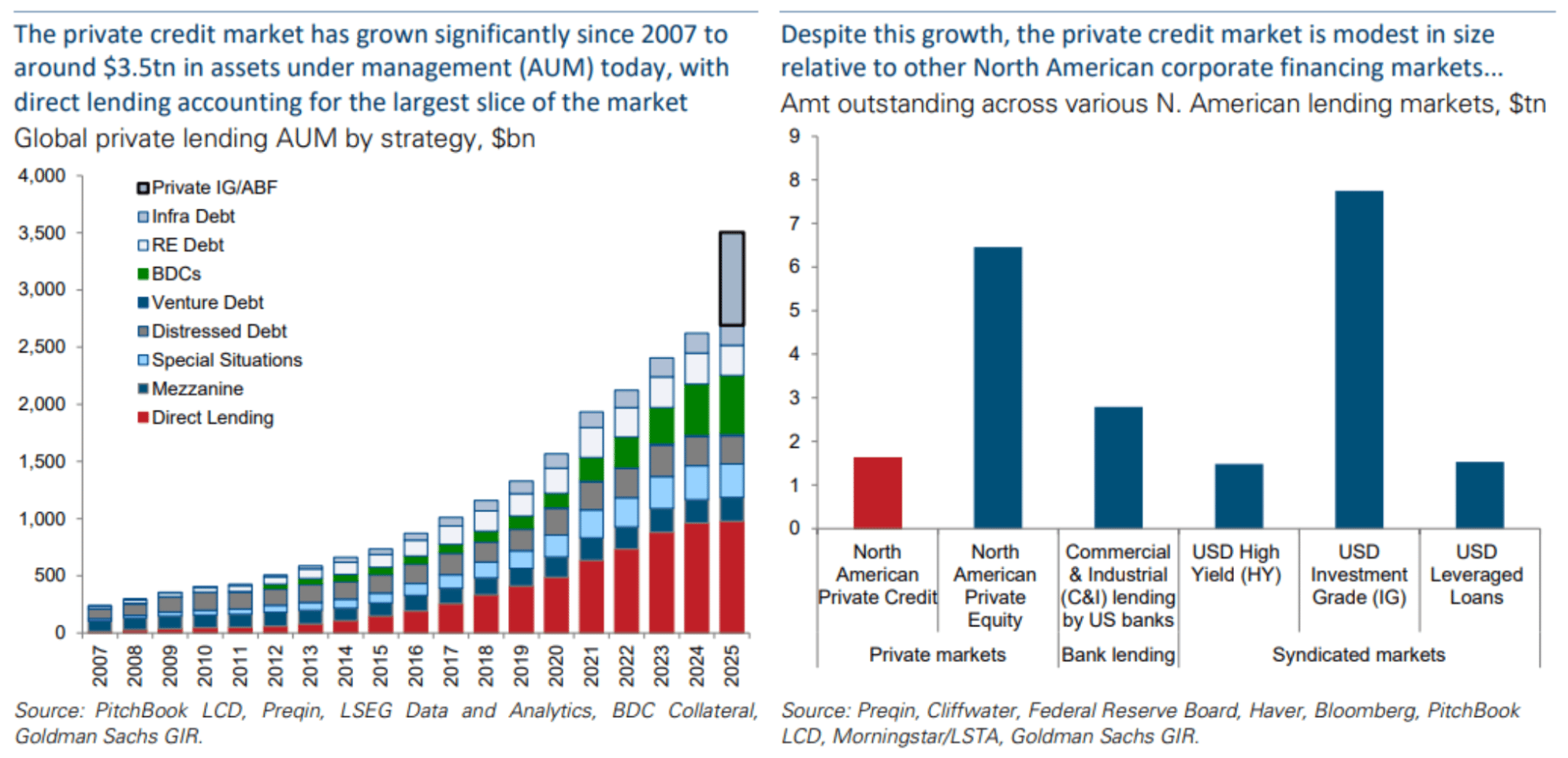

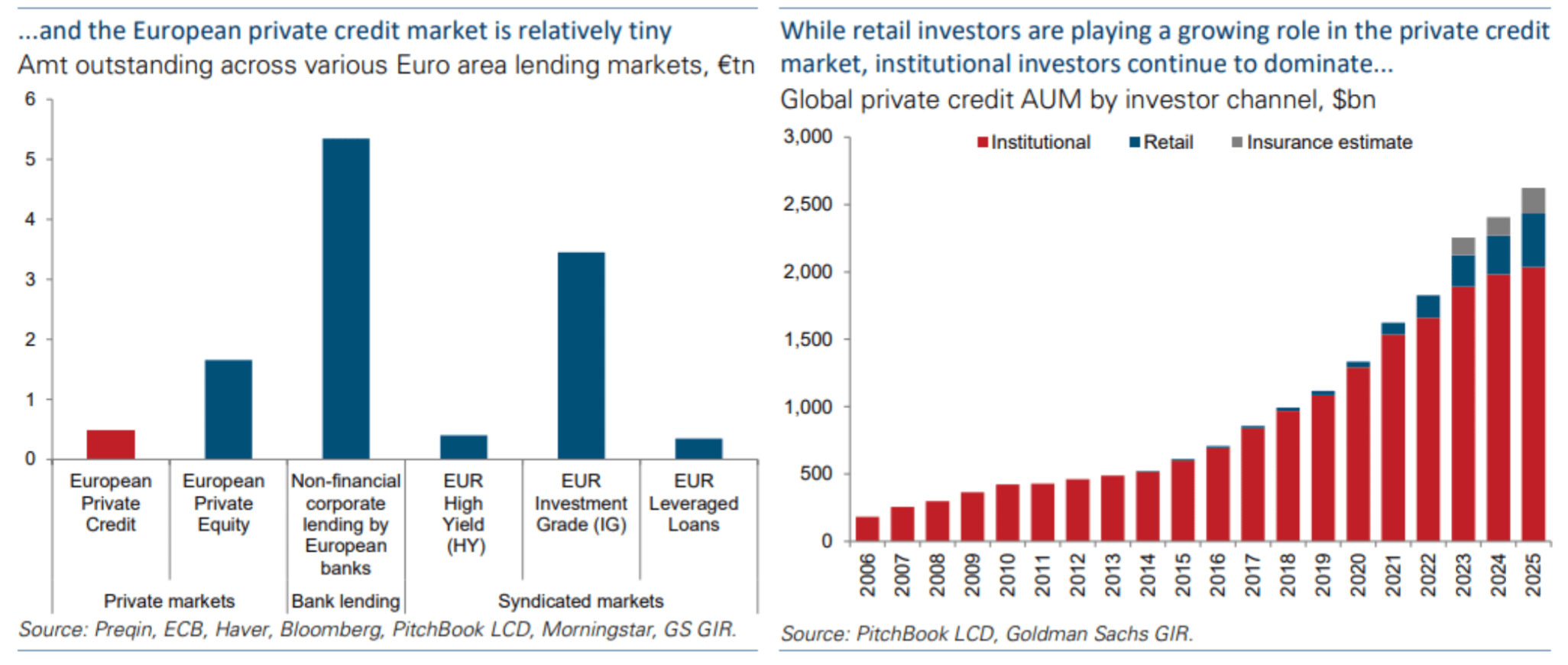

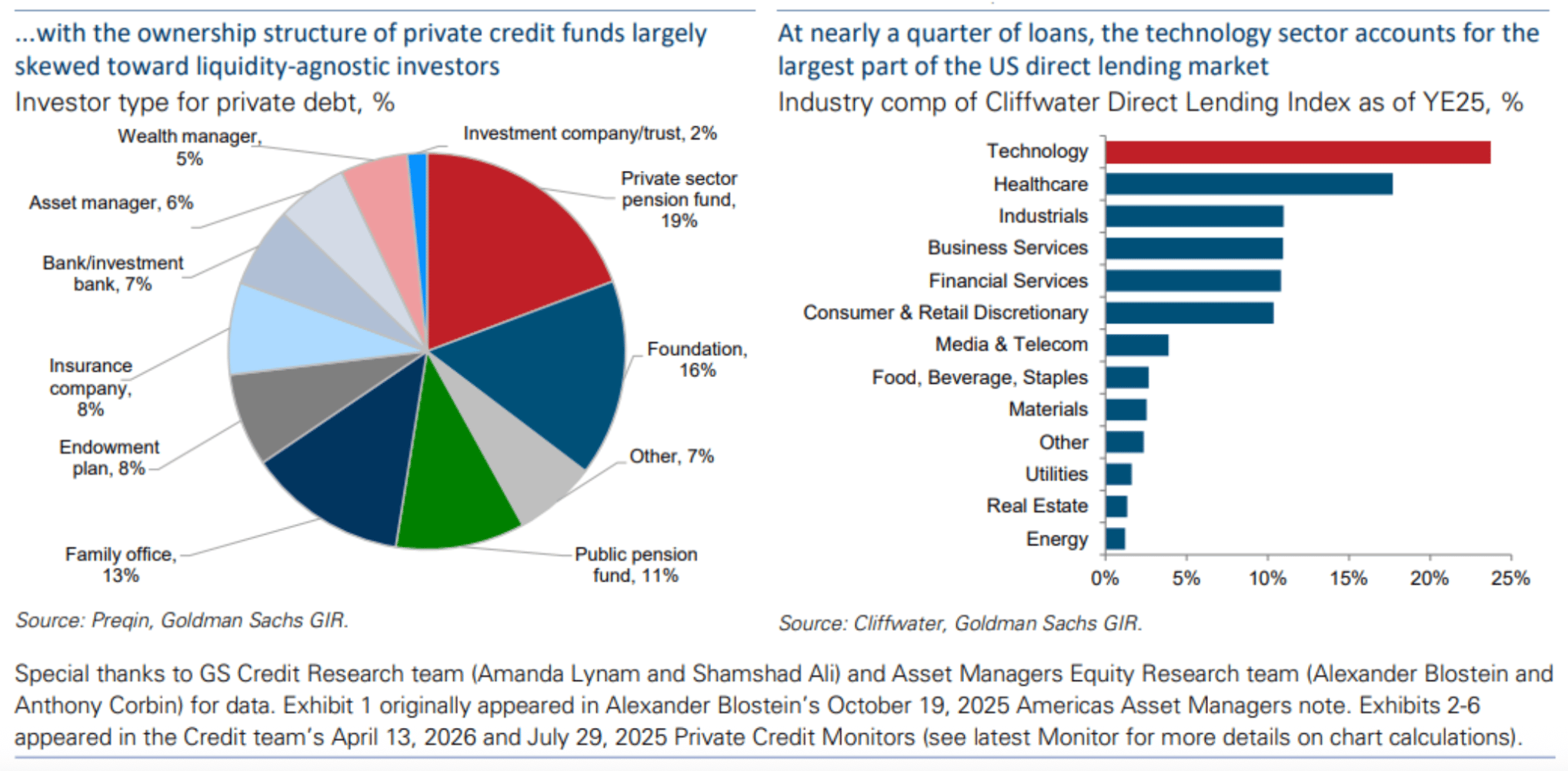

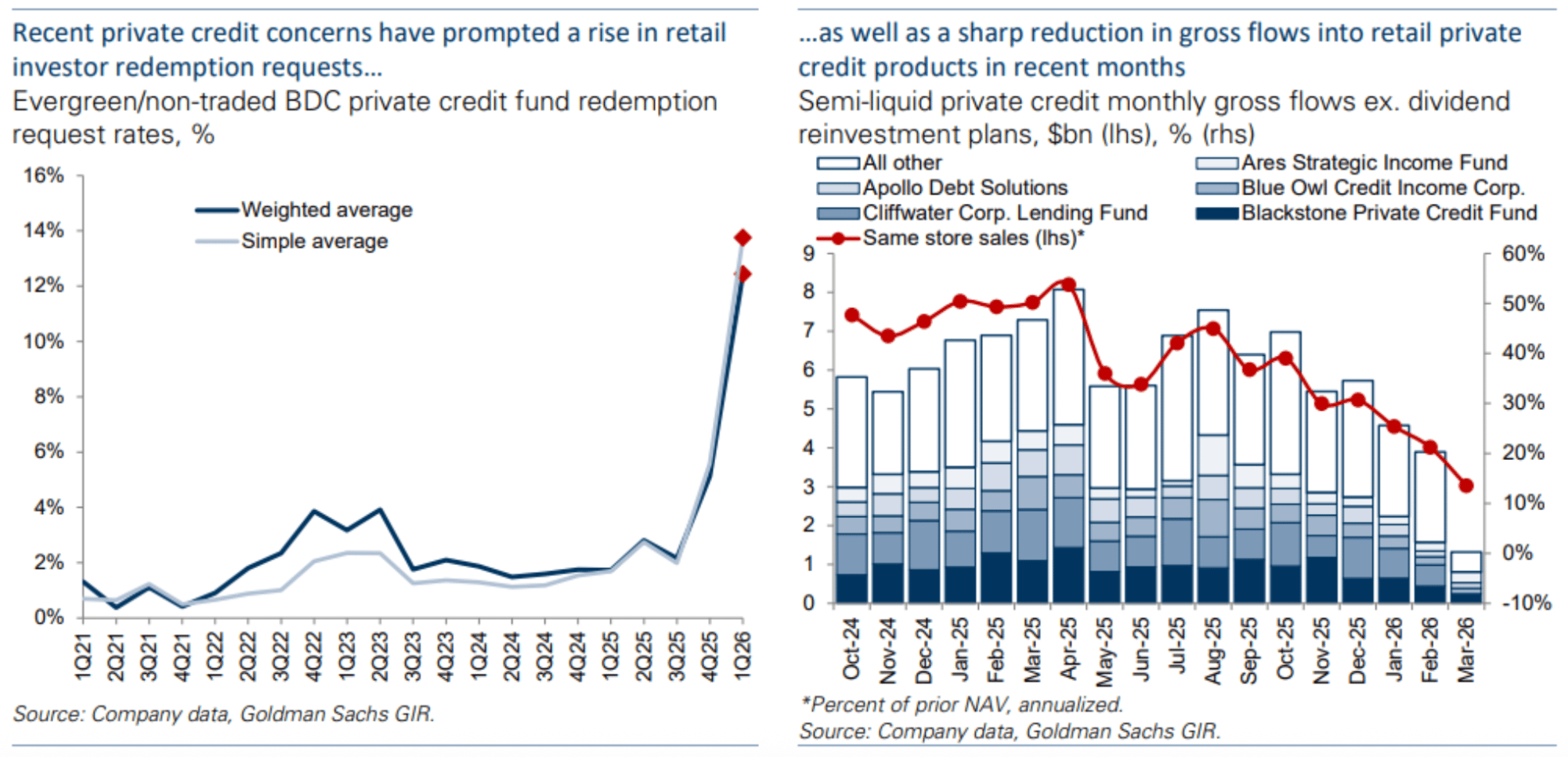

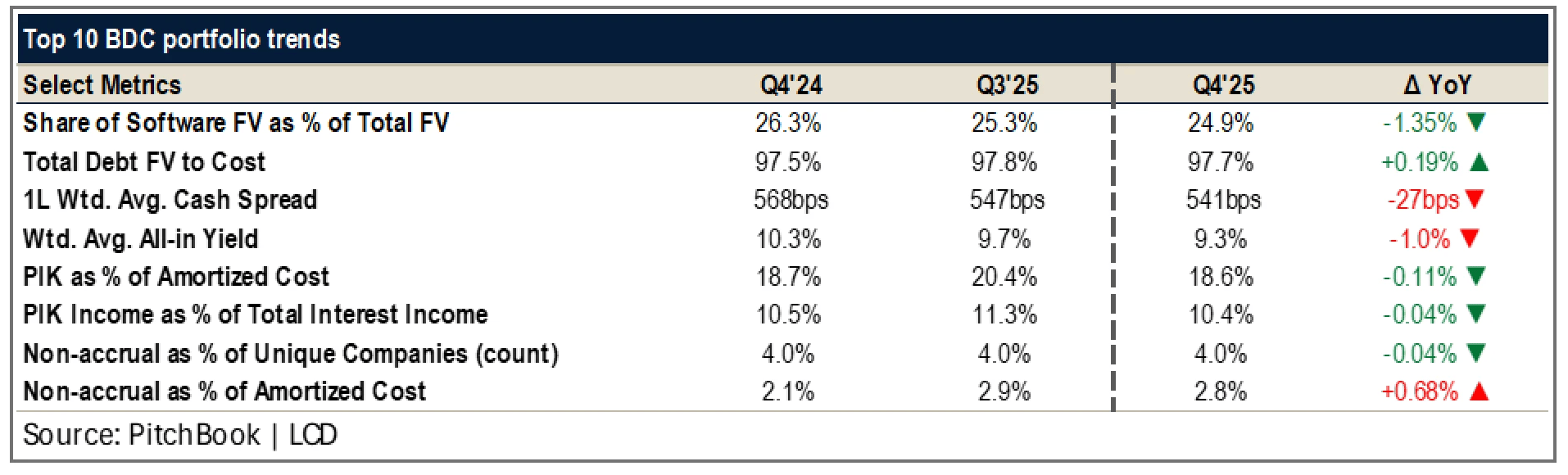

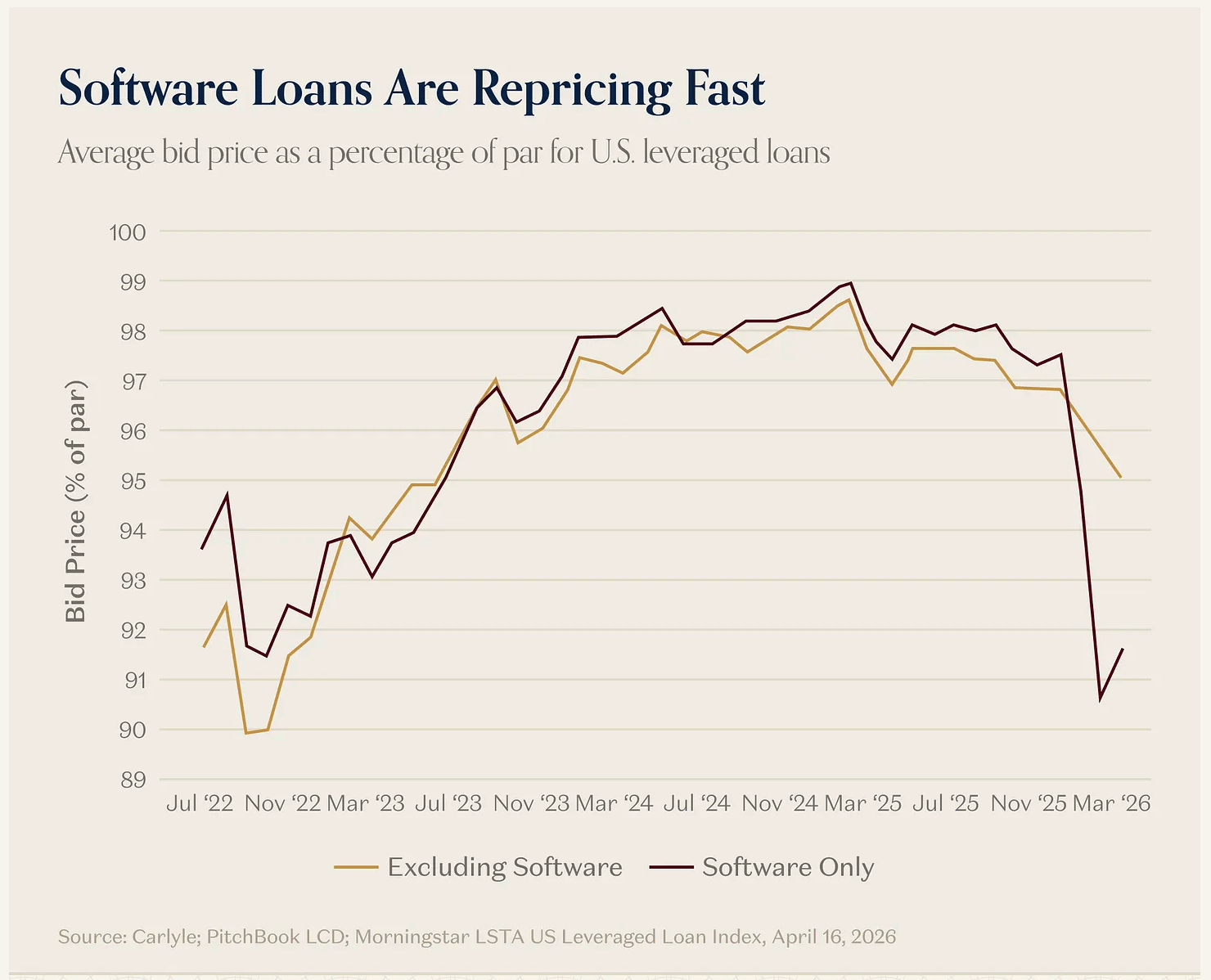

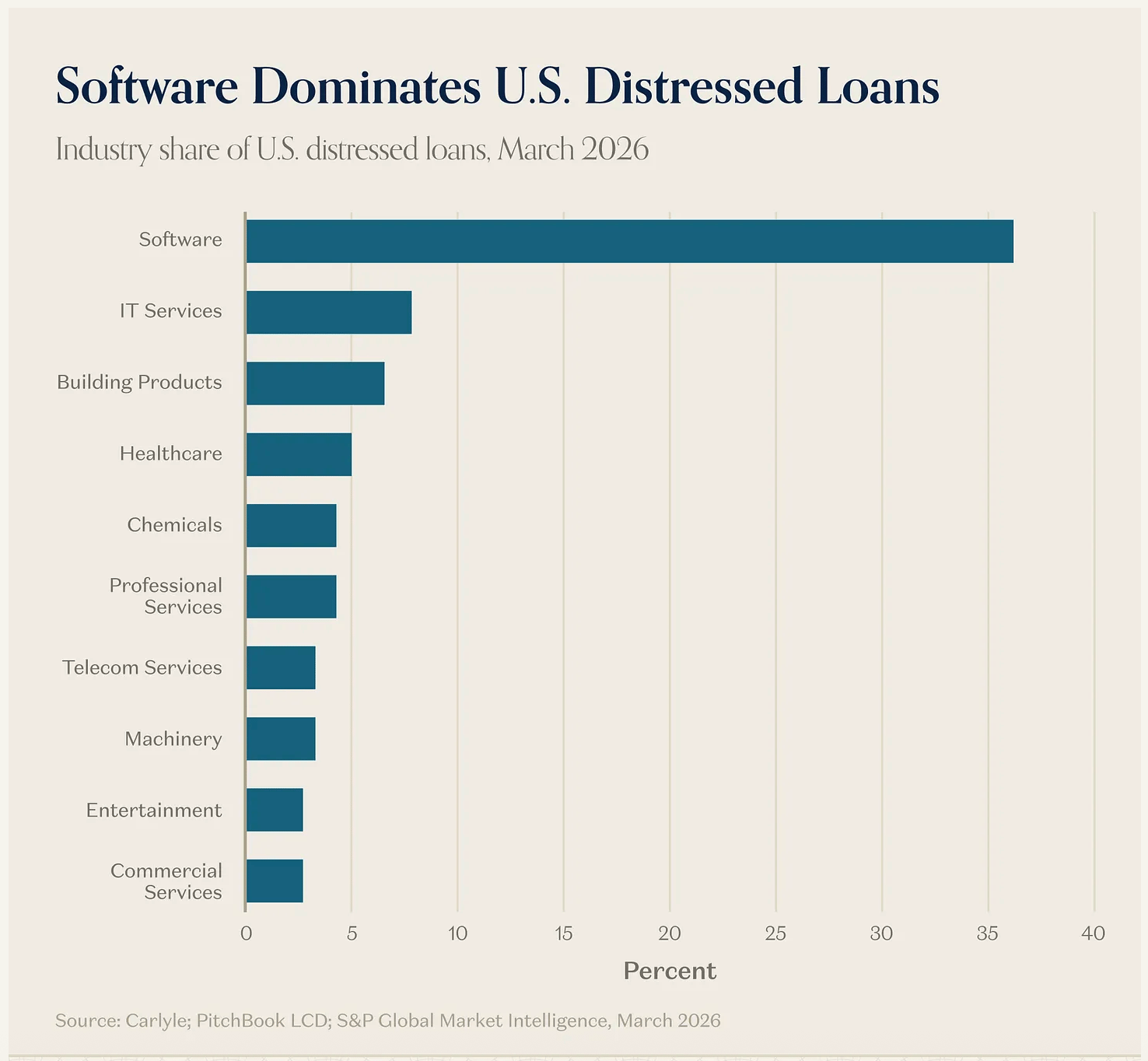

📈 Visuals

🗣️ Market Commentary

“But markets evolve. Private credit was good for a while, yields were 12%. Capital flooded into the market. Yields kept coming down into the mid-to-high single digits for the same risk. But there was so much capital, there was more competition for deals so you also lost covenants and things like that. The kind of capital that started to be raised - retail money - where it comes in one month and it has to be invested right away or you have negative drag, means you kind of have to buy the market what’s out there. One of great things about drawdown funds is if there’s nothing good to do, I don’t have to do anything. You kind of lost that. I think there will be some correction in private markets but it won’t be 2008 because it's not owned by banks at 30-1 leverage. I think one of the great opportunities right now is there are about 30,000 portfolio companies of mid-market private equity firms that can’t be sold and can’t go public - $20T or something worth of value. All of those companies will eventually need to be sold. For capital pools, there’s going to be an immense attractive opportunity to pick company by company - whether it’s co-investments or CVs. I think it’s one of the great times to put money to work.” - Tony James, former President and COO of Blackstone on Evolution of Private Markets

“The real issue here is the liquidity mismatch between the retail investor and the duration of the investments. We live in a world where retail investors have become accustomed to having immediate liquidity for their investments . . . investing in private credit is a different story. Retail was viewed as a phenomenal channel from which to raise assets. But did the retail investors really understand the nature of the investment they were making?” - Ken Griffin, CEO of Citadel on private credit and liquidity

“Retail clearly is going to stop fueling the growth in AUM for private credit. There’s an increasing realization it’s an institutional product, not a retail product. There will be nicks and bruises along the way. Underwriting standards are tightening up.” - Paul Taubman, CEO of PJT on Waning Retail Appetite for Private Credit

“So, valuing assets fairly is a hornet's nest, and especially so for private assets that have no reference point. Private asset investors must therefore accept that there is no correct answer, and no one answer, when it comes to a loan’s fair value. The only way to avoid the inherent unfairness that the uncertainty around NAVs introduces would be to pay investors leaving the fund the proceeds the manager receives when they sell off the departing investor’s share of the assets. But that’s not how these vehicles are structured.” - Howard Marks, Chairman of Oaktree on structural challenges with private asset valuations

“Over the last several years because of the same dynamics of the GFC, regulations, because bank balance sheets are full, they’ve pulled out of some areas. They’ve gotten less aggressive. Real estate being one of them - significantly. Because look at office buildings, vacancy rates, Chicago, New York, San Francisco. Banks have lots of real estate on the balance sheet, so they’re less inclined to put more on. That’s generated an opportunity for private credit. Our real estate private credit has increased five-fold over the last three years. That’s one area of alternative private credit. The second area is just good old fashion specialty finance. Consumer finance, buying pools of receivables, healthcare receivables, SPV lending, litigation finance, royalty financing, drug financing, venture debt financing. Areas where it hasn’t been core but it was niche. Those niches are becoming core. Where investors expect to find excess return is in private credit. It’s our job as managers to find that excess return and alpha. We think today one of the best areas today for alpha is alternative credit.” - Ted Koenig, Chairman and CEO of Monroe Capital on Core Opportunities in Alternative Private Credit

📖 What We’re Reading & Listening To

Earnings & Investor Presentations

Reading

AI isn’t coming for your job. It’s coming for your mind. (Baillie Gifford)

Banks Get Picky on Asset-Based Lending After Credit Blow-Ups (Bloomberg)

Cracks in Private Credit (GS)

Credit Currents (BlackRock)

Echoes of Junk Bonds Past (Verdad)

Mexico’s Banks Handed Out Millions of Cards That Nobody Wants (Bloomberg)

Private Credit Boom Pushes Fund Finance Market Past $1 Trillion (Bloomberg)

The Coming FinTech Liquidity Supercycle (FT Partners & Blue Dot Investors)

Podcasts & Interviews

Building Blackstone, Backing Costco, with Tony James (a16z)

Convergence: Finding Opportunity in a Converging Credit Market (Apollo)

Drew McKnight, Co-CEO of Fortress, Discusses All Things Credit (Capital Creek Partners)

Jamie Dimon, CEO JPMorgan Chase: Corporate culture, risk, and the global economy (In Good Company)

Legends Live @ Citi: Josh Harris (Citi)

Private Credit in the Institutional Portfolio: Ted Seides, Ted Koenig, Rick Miller, Bouk van Geloven, Jeff Levin, Megan Neuberger (Milken Institute Global Conference 2026)